Money Management for Beginners:

Simple Daily, Weekly & Monthly Steps to Build Wealth

Why Most People Struggle With Money (And How to Fix It)

Let’s be honest. Nobody teaches you this stuff in school. You learn algebra and the history of ancient Rome, but you graduate without knowing how to read a payslip, what an emergency fund is, or why carrying a credit card balance is quietly destroying your future wealth.

That’s not your fault. But it is your problem to fix — and the good news is, it’s way simpler than the finance industry wants you to believe.

The secret is systems, not willpower. The people who are great with money don’t have more discipline than you. They’ve built habits and automations that make smart money decisions the default. This guide shows you exactly how to do that — starting today.

| ✏️ HUMAN EXPERT INSERT REQUIRED [INSERT PERSONAL STORY] — Share a real moment when you felt out of control with money. An overdraft, a credit card bill that shocked you, or the first time you actually looked at your spending and felt sick. This vulnerability hooks readers immediately and establishes that you understand what they’re going through. Keep it to 3–4 sentences. |

Step 1: Know Where Your Money Goes (Tracking)

Before you budget, save, or invest a single penny — you need to know where your money is actually going. Most people think they know. Most people are wrong.

Studies consistently find that people underestimate their discretionary spending by 20–30%. That takeaway coffee, the random Amazon purchase, the subscription you forgot about — it all adds up silently.

How to Start Tracking in Under 5 Minutes

- Download a free expense tracking app. YNAB (You Need A Budget), Mint, or PocketGuard are all good starting points. Even a basic spreadsheet works fine.

- Link your bank account or credit card so transactions import automatically — or log manually each evening (takes 2 minutes).

- Do this for 30 days without changing anything. Just observe. The awareness alone will change your behaviour.

- At the end of the month, categorise your spending: housing, food, transport, entertainment, subscriptions, etc.

- Look for surprises. There will be at least one category that shocks you.

| 💡 The 2-Minute Daily Habit Every morning, open your banking app and skim yesterday’s transactions. This one tiny habit — just 2 minutes — keeps you fully aware of your spending patterns all week long. It also catches billing errors and fraud fast. |

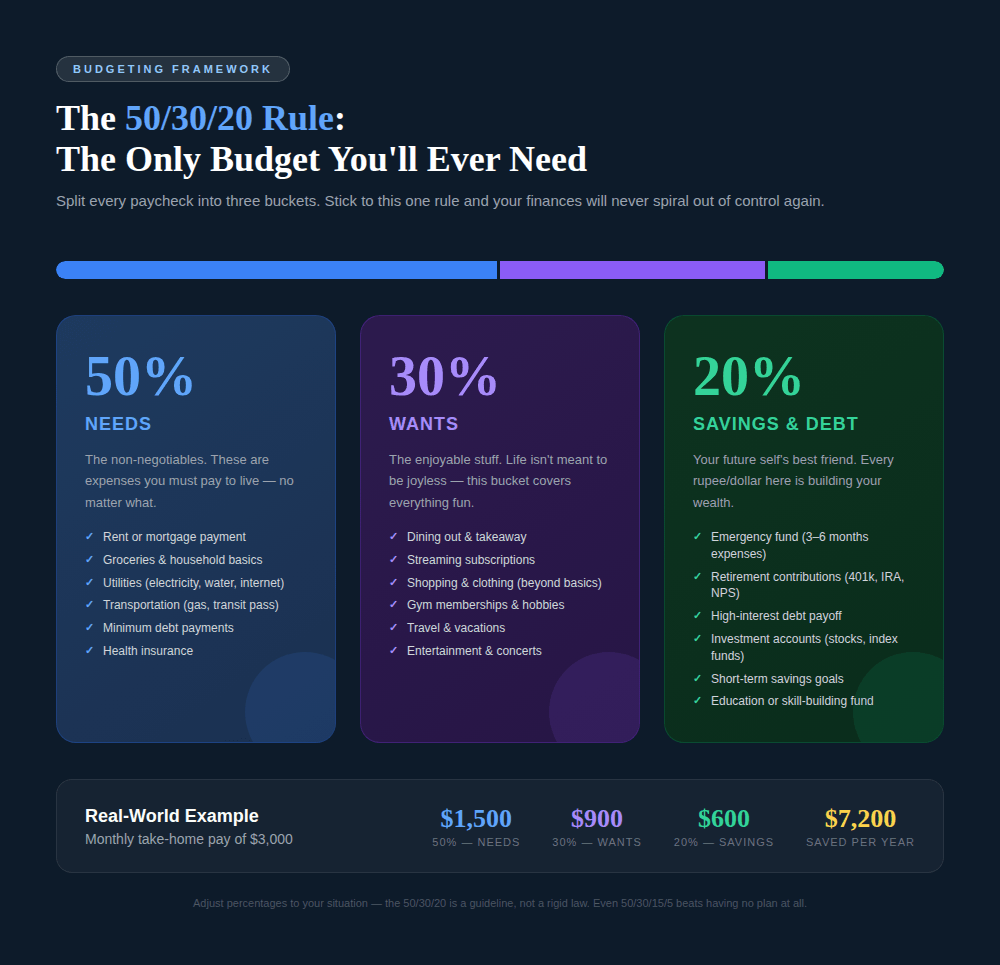

Step 2: Set a Budget That You’ll Actually Stick To

The word ‘budget’ makes people think of restriction and misery. Flip that thinking. A budget isn’t a prison — it’s a spending permission slip. It tells you exactly how much you’re allowed to enjoy guilt-free.

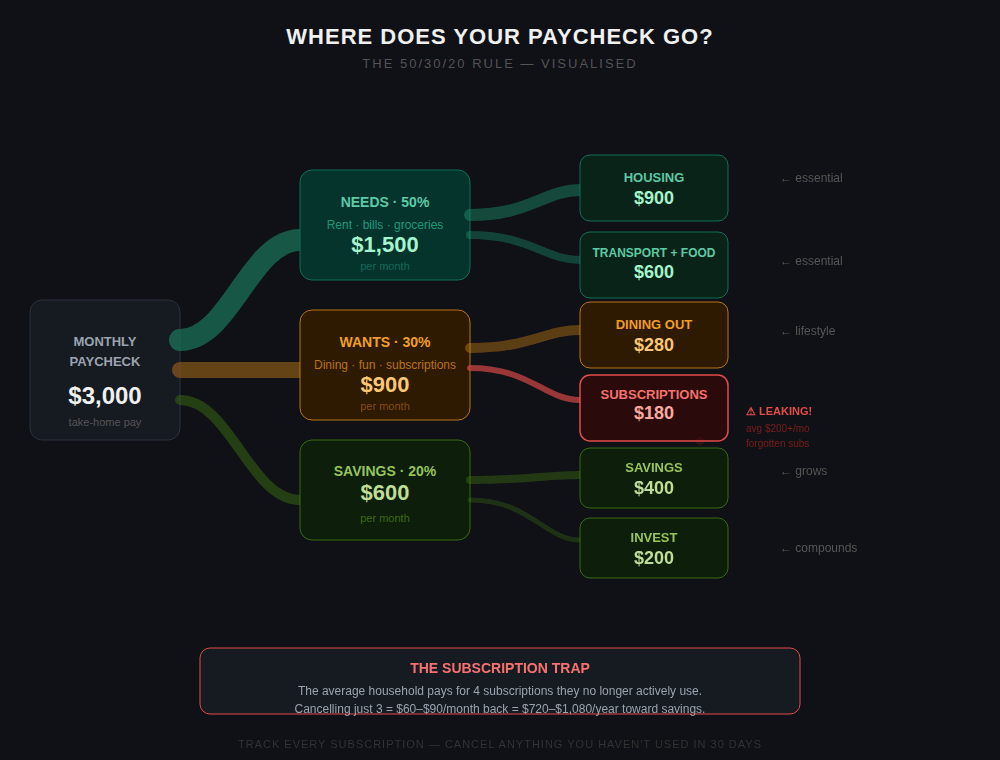

The simplest budgeting framework for beginners is the 50/30/20 rule. You split your take-home pay into three buckets:

What If My Numbers Don’t Match Up?

If your ‘needs’ are consuming more than 50% of your income, you have two options: cut fixed costs (downsize housing, refinance debt, switch energy providers) or increase income. If your ‘wants’ are eating 50%+ and you want to save more, start by cutting the three lowest-value subscriptions or habits.

A note on perfectionism: don’t wait until your budget is perfect before you start. An imperfect budget you actually follow beats a perfect spreadsheet you abandon after a week. Start messy. Refine over time.

Best Free Budgeting Apps in 2026

| App | Best For |

| YNAB (You Need A Budget) | Best overall — proactive budgeting, syncs with banks |

| Mint / Credit Karma | Free, auto-categorises spending, credit score tracking |

| PocketGuard | Shows ‘safe to spend’ amount after bills & goals |

| Copilot | Beautiful UI, AI-powered insights (iOS) |

| Excel / Google Sheets | Most flexible — free if you’re comfortable with spreadsheets |

| Emma (UK) | Great for UK users, tracks all accounts in one place |

Step 3: Build Your Emergency Fund First

Before you pay off extra debt. Before you invest. Before you do anything else — build an emergency fund. This is the single most important first step in money management, and most people skip it.

An emergency fund is 3–6 months of living expenses held in a separate, easily accessible high-yield savings account. It is not for holidays. It is not for sales. It exists for one reason: so that a job loss, car breakdown, or medical bill doesn’t send you into debt.

| 🛡️ Why This Comes Before Investing People skip the emergency fund to invest faster — then pull money out of their investments when life happens, often during a market dip. You lock in losses AND pay penalties. A boring savings account is the foundation that lets everything else work. |

How to Build Your Emergency Fund Fast

- Open a separate high-yield savings account. Not your main account — separation is the key.

- Start with a mini goal of $500–$1,000. This covers the most common emergency (car repair, small medical bill) and feels achievable.

- Automate a weekly or monthly transfer — even $25/week adds up to $1,300 a year without you thinking about it.

- Put any windfalls (tax refund, birthday money, bonus) directly here until fully funded.

- Once you have 3–6 months saved, move the fund to the highest-yield account you can find. Check MoneySavingExpert (UK) or NerdWallet (US) for current best rates.

Step 4: Tackle Debt With a Clear Strategy

Not all debt is equal. A mortgage at 4% interest is very different from a credit card at 22%. Getting these straight in your head changes everything.

| Concept | What It Means |

| Good debt (generally) | Mortgage, student loan, low-interest car loan — debt that builds assets or earns you more than it costs |

| Bad debt (tackle first) | Credit cards (18–29% APR), payday loans, buy-now-pay-later balances, high-interest personal loans |

| Debt snowball method | Pay off your smallest debt first for quick wins, then roll that payment to the next. Motivating. |

| Debt avalanche method | Pay off your highest-interest debt first. Saves the most money overall. Less emotionally satisfying but mathematically superior. |

| Which to choose? | Snowball if you need motivation. Avalanche if you’re disciplined. Either one beats no plan. |

One hard rule: always pay the minimum on every debt every month. Missing payments wrecks your credit score and triggers penalty fees. Beyond the minimum, focus all extra cash on your target debt using whichever strategy you chose.

For consolidating multiple debts, compare options at MoneySuperMarket (UK) or Bankrate (US) — but only if you can get a meaningfully lower interest rate.

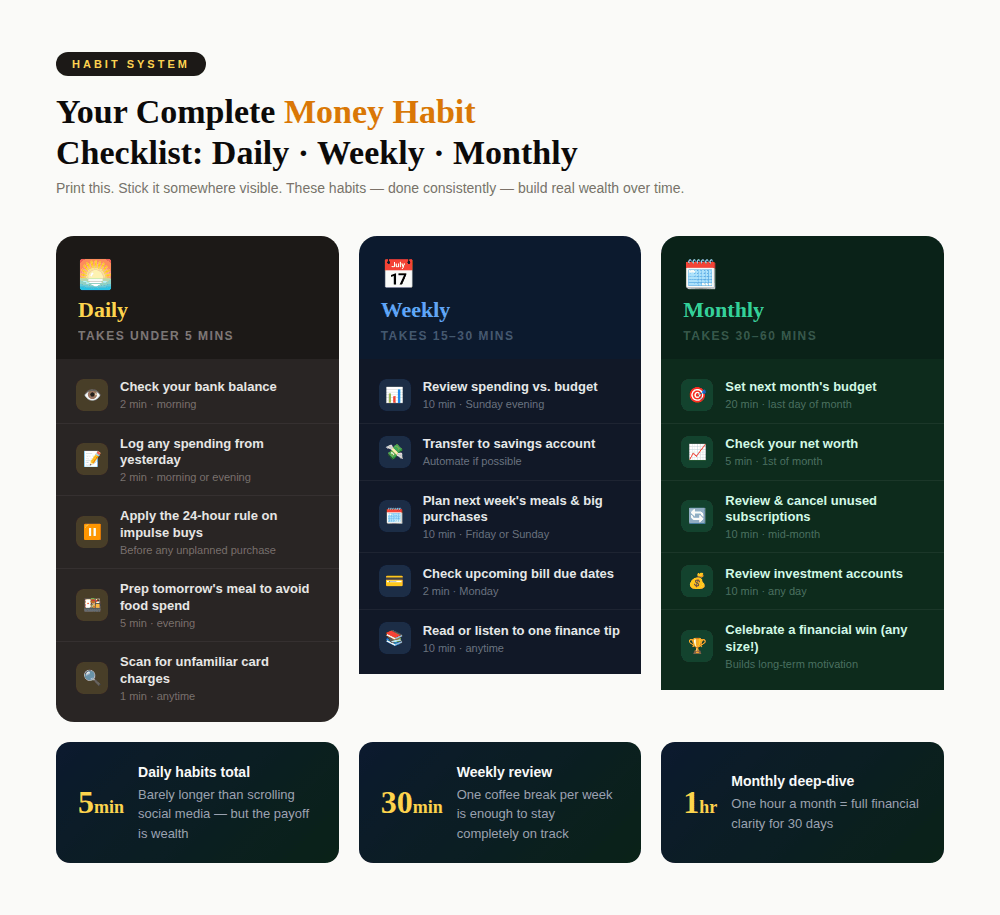

Your Money Habit System: Daily, Weekly & Monthly

Knowing what to do matters. But the real magic is making these habits automatic — so you don’t have to think about them.

The Automation Stack — Set It and Forget It

The most powerful thing you can do for your finances is reduce the number of decisions you have to make. Here’s the automation sequence that top personal finance experts recommend:

- Payday automation: Set up automatic transfers on the same day your salary arrives. Savings go out before you can spend them.

- Bill pay: Automate every regular bill. Never pay a late fee again.

- Investing: Set up recurring investments into an index fund or retirement account. Start with whatever you can afford — even £/€/$20/month.

- Debt payments: Automate at least the minimum on every debt. Set a higher amount on your target debt.

| ⚡ The Pay-Yourself-First Rule Move savings to a separate account the moment you get paid — before you pay bills, before you buy groceries, before you do anything. This one psychological trick is responsible for more wealth-building than almost any other habit. When you save what’s ‘left over,’ there’s never anything left over. |

Step 5: Start Investing (Even With Small Amounts)

Once your emergency fund is in place and your high-interest debt is under control, it’s time to make your money work for you. This is where real wealth gets built.

Investing doesn’t require a financial advisor or a large lump sum. The most beginner-friendly approach is to invest regularly in a low-cost index fund — a single investment that tracks hundreds of companies at once, spreading your risk automatically.

Where to Start Investing as a Beginner

- In the UK: Open a Stocks & Shares ISA (up to £20,000/year, tax-free). Vanguard, Moneybox, and InvestEngine are beginner-friendly.

- In the US: Open a Roth IRA or contribute to your employer’s 401(k) — especially if they offer a match. Fidelity, Charles Schwab, and Vanguard US all offer zero-fee index funds.

- Global options: Interactive Brokers and eToro are available in many countries for low-cost global investing.

What to Actually Invest In

For beginners, you need exactly one investment: a broad global index fund. Something like the Vanguard FTSE Global All Cap (UK) or Vanguard Total World ETF (VT) (US). That’s literally it. One fund, diversified across thousands of companies worldwide. Set up a monthly contribution. Stop checking it daily.

| ⚠️ Investing Disclaimer Investing involves risk and the value of investments can go down as well as up. This article is for informational purposes only and is not personal financial advice. Speak to a qualified financial advisor before making investment decisions. |

10 Quick Money Wins You Can Do This Week

Don’t know where to start? Do these. Each one takes less than 30 minutes and will immediately improve your financial health.

- Check your bank balance right now. Awareness is step one.

- List every subscription you pay for. Cancel anything you haven’t used in 30 days.

- Open a dedicated savings account. If you don’t already have one separate from your everyday account, do this today.

- Set up one automatic saving transfer. Even $25 or £25 a week counts.

- Download a budget app. YNAB or Mint — start tracking for free.

- Check your credit score for free. ClearScore (UK/global) or Credit Karma (US) — free, won’t affect your score.

- Negotiate one bill. Call your internet, mobile, or insurance provider and ask for a better rate. Switching or threatening to switch works over 50% of the time.

- Find your employer’s pension/retirement match. If your employer matches contributions and you’re not contributing enough to get the full match, you’re leaving free money on the table. Fix this first.

- Set a ‘no-spend’ day this week. One full day of zero discretionary spending. It resets your habits and usually feels liberating.

- Tell someone your financial goal. Accountability is one of the most powerful financial tools that nobody talks about. Tell a trusted friend one money goal you’re working on.

FAQ: People Also Ask

Formatted for Google’s ‘People Also Ask’ boxes. Add FAQ schema markup in your CMS for each question below.

How should a beginner start managing their money?

Start with three steps: (1) Track your spending for 30 days using a free app like YNAB or Mint to see exactly where your money goes. (2) Set up a simple budget using the 50/30/20 rule — 50% for needs, 30% for wants, 20% for savings and debt. (3) Automate a savings transfer to a separate account on payday. These three steps alone put you ahead of most people.

What is the 50/30/20 rule?

The 50/30/20 rule is a budgeting framework where you allocate 50% of your take-home pay to needs (rent, groceries, bills), 30% to wants (dining, entertainment, subscriptions), and 20% to savings and debt repayment. It was popularised by US Senator Elizabeth Warren in her book All Your Worth. It’s an excellent starting point because it’s simple enough to remember and flexible enough to adapt.

How much should a beginner save each month?

Aim to save at least 10–20% of your take-home pay each month. If that’s not possible right now, start with whatever you can — even 1–2% is better than nothing. The habit matters more than the amount early on. As your income grows or your expenses reduce, increase your savings rate gradually. Most financial experts suggest working toward a 20% savings rate as a long-term goal.

What should I do with my first £1,000 / $1,000 in savings?

Keep your first $1,000 in a high-yield savings account as the foundation of your emergency fund. Do not invest it yet. Life will throw an unexpected expense at you, and having this buffer means you won’t need to go into debt or raid investments when it happens. Only after you have a full 3–6 month emergency fund saved should you consider investing.

What is the best budgeting app for beginners?

For most beginners, YNAB (You Need A Budget) is the gold standard — it’s proactive rather than reactive, meaning it helps you plan spending before it happens rather than just tracking it after. It has a learning curve but a free 34-day trial. For a completely free option, Mint (US) or Emma (UK) are excellent starting points that sync automatically with your bank accounts.

How do I stop living paycheck to paycheck?

Breaking the paycheck-to-paycheck cycle requires four things: (1) Track spending to find where money is leaking. (2) Cut or reduce 2–3 expenses immediately — subscriptions and takeaway food are the easiest targets. (3) Build a small $500 emergency buffer to stop emergencies from pushing you into overdraft. (4) Automate a savings transfer, even $50/month, so savings happen before spending. It’s a slow process but these four steps are the proven path out.

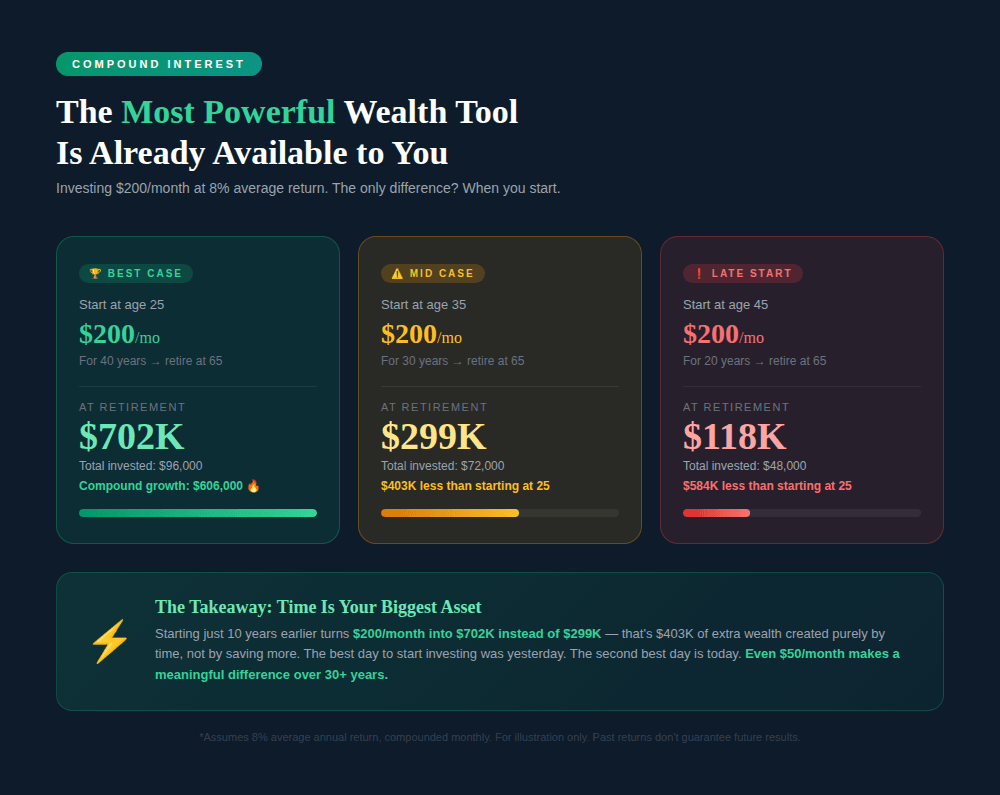

When should I start investing?

Start investing after you have: (1) a full emergency fund of 3–6 months of expenses, and (2) paid off all high-interest debt (credit cards, payday loans). Once those two conditions are met, begin investing — even small amounts — as early as possible. Time in the market beats timing the market. Thanks to compound interest, £100 invested at age 25 is worth significantly more than £100 invested at age 45.