101 Frugal Living Tips to Save $1,000 a Month

How did frugal living enter your life? As a student with a tight budget, what forced you to start paying attention to spending? A specific number or moment — “I checked my bank account and had £47 left for three weeks” — is worth more than any amount of general advice. This is the opening that keeps people reading.

Let’s start with what “saving $1,000 a month” actually means, because the headline sounds big until you see how it works.

I study digital marketing, which means I spend a lot of time understanding how companies design experiences to make you spend. The subscription that renews silently, the one-click purchase flow that removes all friction, the “limited time only” banner on a product that’s been on sale for six months — I know what these are doing, and knowing helps. That’s a thread I’ll pull through this guide: not just what to do, but why the opposite behaviour keeps costing you money.

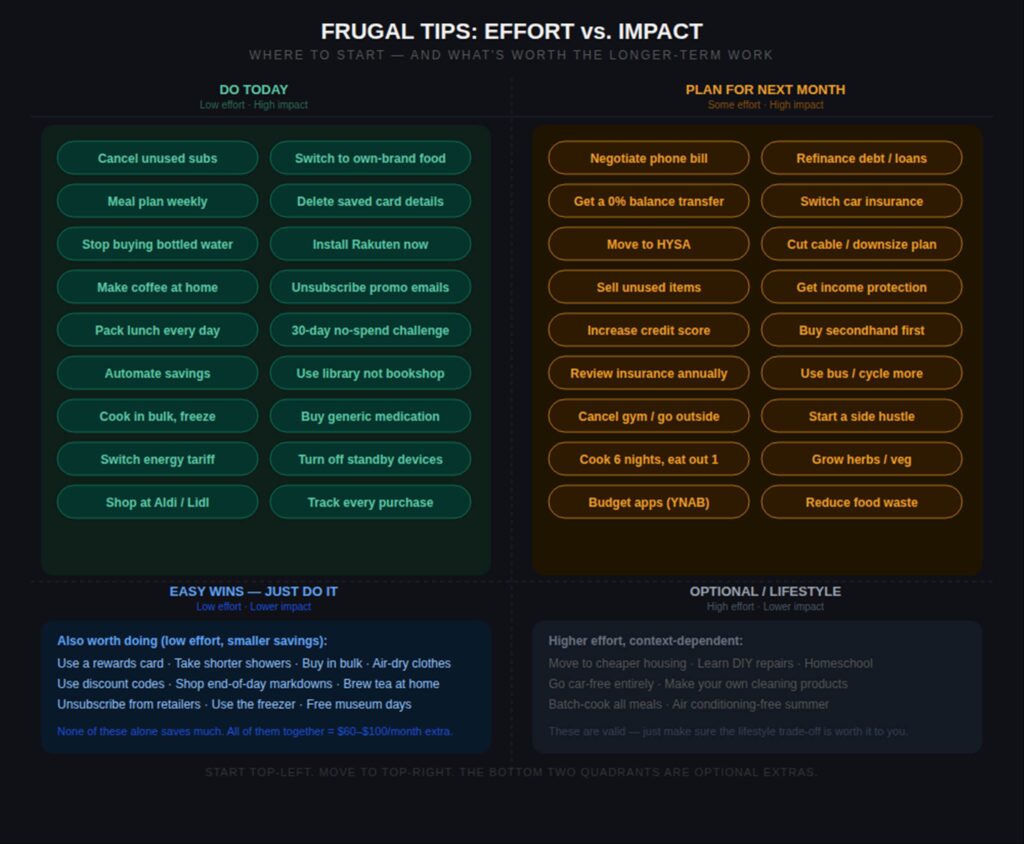

The effort-impact matrix below shows which tips to do today versus which to plan for next month. Start there.

Here are 101 frugal living tips, grouped by category, with honest commentary on the ones worth prioritising first.

Food and Groceries — Save $150–$200/Month

Food is consistently the single largest discretionary spending category for most households — and it’s the one with the most room to move. I’m not talking about eating badly. I’m talking about being strategic about where and how you buy.

1. Shop at discount supermarkets first

Aldi, Lidl, and store-brand heavy supermarkets consistently price staples 20–40% below premium chains. My grocery bill dropped by about a third when I made Aldi my default. I still go elsewhere for specific things I can’t find there — but they’re my first stop.

2. Meal plan before every shop

This is the single highest-impact food tip on this list. Without a plan, you buy vague ingredients and end up ordering delivery mid-week anyway. With a plan, you buy exactly what you’ll use. I plan on Sunday mornings — takes 15 minutes.

3. Write a list and stick to it

Supermarkets are deliberately designed to maximise unplanned purchases. Eye-level placement, end-of-aisle offers, the bakery smell near the entrance — all of it is engineered. A list is your defence against their floor plan.

4. Buy own-brand for basics

Flour, butter, milk, eggs, rice, pasta, tinned tomatoes, olive oil — there is no meaningful quality difference between the own-brand and the premium version for most of these. The price difference is real: typically 30–60% less.

5. Cook once, eat twice (or three times)

Batch cooking isn’t just a time-saver — it’s a waste reducer. A pot of soup, a tray of roasted veg, a big batch of rice: these become two or three meals throughout the week rather than one. My food waste dropped significantly when I started cooking with leftovers intentionally.

6. Use your freezer properly

The freezer is the most underused appliance in most kitchens. Bread, meat, cooked meals, soups, herbs, overripe bananas for smoothies — most things freeze. Throwing food away is literally throwing money in the bin.

7. Eat before you shop

This is backed by actual behavioural research, not just common sense. Hungry shoppers make more impulse purchases. Eat something, then go. The difference on your receipt is measurable.

8. Shop the reduced aisle

End-of-day markdowns on meat, dairy, and bakery items are often 50–75% off. I’ve built whole meals around whatever was reduced. The food is perfectly fine — it just needs using that day or freezing.

9. Stop buying pre-cut and pre-prepared

A bag of pre-washed salad costs three times what a whole lettuce costs. Pre-cut butternut squash costs four times the whole one. Convenience pricing is real and significant. Ten extra minutes of chopping saves £30–£40/month.

10. Make your own coffee at home

A £4 coffee bought five days a week is £80/month. A bag of decent ground coffee at home is £5/month. I made this switch at university and I don’t miss the coffee shop — I just don’t go as often, which means when I do, it feels like a treat rather than a habit.

11. Reduce meat consumption by two dinners a week

Meat is the most expensive ingredient in most meals. Two meat-free dinners a week — lentil soup, egg fried rice, pasta e fagioli — saves £20–£40/month and takes no culinary skill.

12. Stop buying bottled water

In most Western countries, tap water is clean and safe. A reusable water bottle costs £10. The average person who buys bottled water daily spends £30–£50/month. This one is simple, immediate, and has zero quality trade-off.

The $150–$200/month food saving doesn’t require eating worse — it requires shopping differently. Most of the saving comes from switching to Aldi, buying own-brand, and reducing waste. Those three alone account for the majority.

Subscriptions and Bills — Save $100–$150/Month

This is the category where money disappears most invisibly. From a digital marketing perspective, subscription businesses are explicitly designed around the fact that people forget to cancel. The “easy sign-up, hard to cancel” model is a business strategy, not an accident.

13. Do a full subscription audit

Go through your last three bank statements and highlight every recurring charge. Most people find 4–8 subscriptions they’d forgotten about. My honest count when I first did this: two streaming services I hadn’t opened in months, a meditation app, and a cloud storage plan I’d duplicated. That was £30/month for nothing.

14. Share subscriptions where allowed

Netflix, Spotify, Amazon Prime, Disney+ — most allow family or household sharing within their terms. Split costs with housemates, family, or a trusted friend. A £17.99/month plan split two ways is £9/month.

15. Downgrade plans you don’t fully use

Are you paying for the 4K streaming plan on a laptop? The unlimited data plan you never fully use? The premium gym membership when you go twice a week? Downgrading to a plan that matches actual use saves money with no real change in experience.

16. Call your providers to negotiate — every year

This is one of the highest-return-per-hour actions on this list. Call your broadband provider, mobile network, and insurance company around renewal time and say you’re thinking of leaving. New customer deals are almost always better than the loyalty rate. You will often be offered a discount without even fully committing to leave.

17. Switch energy supplier

18. Cut cable TV or downsize your package

The average cable TV bill in the US is over $100/month. A combination of one or two streaming services covers most of what people actually watch for a fraction of that. I haven’t had cable in years and I’ve never missed a thing I actually wanted to see.

19. Cancel gym membership and exercise outdoors

Running is free. Bodyweight training is free. A yoga mat costs £20. If you’re using your gym five times a week, this tip doesn’t apply. If you’re going twice a week, the cost-per-session maths is brutal.

20. Switch to a free banking account

Most people pay £0 in explicit bank fees but pay significantly in implicit ones: arranged overdraft interest, foreign transaction fees, ATM charges. Review what your bank is actually costing you. Free current accounts with no fees exist at most major banks and challengers.

21. Pay annual subscriptions upfront if cheaper

Most subscription services offer 20–30% off for paying annually rather than monthly. If you know you’ll use it for 12 months, the maths almost always favours annual. Just make sure you actually use it.

22. Check for free alternatives first

undefined free vs Pro. Google Docs vs Word. Spotify free vs Premium. KDEnlive vs Premiere Pro. For most things people pay subscriptions for, a free alternative that’s 80% as good exists. That’s often enough.

Honest note: The subscription audit alone — done properly — typically saves £30–£80/month for most households. It takes 20 minutes. Do it this week before reading anything else on this list.

Transport and Fuel — Save $100–$150/Month

Transport is often the second-largest household expense after housing, and it’s one most people accept as fixed when it isn’t.

23. Walk or cycle for journeys under 2 miles

The average short car trip costs significantly more than people think when you factor in fuel, depreciation, and insurance per mile. Walking or cycling under 2 miles is genuinely free and faster in urban traffic.

24. Use public transport for longer commutes

Car ownership costs the average UK household £3,000–£5,000/year once you add up finance payments, insurance, fuel, tax, MOT, and maintenance. In cities with reasonable public transport, going car-free or car-light saves a remarkable amount.

25. Work from home where possible

Every day working from home eliminates a commute cost. Even two days per week of home working at £5–£10/day commute cost saves £40–£80/month.

26. Maintain your car properly

Correctly inflated tyres improve fuel efficiency by 0.5–3%. A clean air filter improves performance. Keeping on top of basic maintenance avoids expensive repairs. An ounce of prevention, and all that.

27. Buy fuel at supermarket stations

Supermarket fuel stations (Tesco, Sainsbury’s, Asda, Morrisons in the UK) are consistently 3–5p/litre cheaper than branded forecourts. On a 50-litre fill, that’s £1.50–£2.50 saved per tank. Small but consistent.

28. Compare car insurance every year without exception

Staying loyal to a car insurer is almost always more expensive than switching. I haven’t renewed without checking comparison sites in years. The saving on switching is typically £100–£300/year.

29. Carpool for regular commutes

If you commute by car and colleagues live nearby, splitting a journey halves fuel costs instantly. It also reduces wear on your vehicle and parking costs if applicable.

30. Book train tickets in advance

Advance train tickets in the UK can be 40–70% cheaper than walk-up fares for the same journey. The flexibility trade-off is real — you’re committing to a specific train — but for regular planned travel, it’s significant.

Utilities and Energy — Save $80–$100/Month

Energy costs have shifted significantly in recent years. The savings from small habit changes are real but won’t cover the whole gap — structural changes (switching supplier, improving insulation, adjusting thermostat habits) matter more.

31. Turn off devices fully rather than leaving on standby

Devices on standby still draw power. A TV, set-top box, games console, and laptop charger left on standby costs approximately £50–£80/year according to the Energy Saving Trust. Get a smart power strip and turn everything off at the wall overnight.

32. Wash clothes at 30°C instead of 40°C or 60°C

Modern detergents work effectively at lower temperatures. Washing at 30°C uses around 40% less energy than at 40°C. The clothes come out just as clean.

33. Air-dry clothes instead of using a tumble dryer

The tumble dryer is one of the most energy-hungry appliances in the house — typically 2–3 kWh per cycle. Air-drying is free. Even doing this half the time saves £80–£150/year depending on usage.

34. Drop the thermostat by 1°C

The Energy Saving Trust estimates that dropping your thermostat by just 1°C saves approximately 10% on heating bills. You will barely notice the difference. Your bill will.

35. Take shorter showers

A ten-minute shower uses approximately 60 litres of water. A five-minute shower uses 30. Heating that extra water has a cost. For a family of four, shortening showers saves £50–£100/year.

36. Only boil the amount of water you need

Filling the kettle to the top every time when you only need one cup uses three to four times the necessary energy. Small habit, real saving, zero quality loss.

37. Use LED bulbs throughout

If you haven’t already switched to LED bulbs, do it this week. They use 80% less energy than halogen equivalents and last years longer. A full house switch costs £30–£50 and pays back within months.

38. Monitor your usage with a smart meter

Smart meters give you real-time visibility on energy consumption. Seeing the cost go up in real time when you turn on the oven or tumble dryer changes behaviour in a way that abstract bills don’t.

Infographic: Effort vs. impact matrix — which tips to prioritise and when

Shopping and Spending Habits — Save $100–$130/Month

This is where understanding marketing psychology matters most. I’ve studied how retailers and brands design purchase experiences, and once you see the mechanisms clearly, impulse spending becomes a lot harder to justify.

39. Delete saved card details from every shopping site

Friction reduces impulse purchases. If buying something requires getting your wallet, typing a card number, and waiting, you’ll abandon a significant percentage of unplanned purchases. Saved cards remove that friction deliberately. Remove them deliberately in return.

40. Implement the 48-hour rule for non-essential purchases

Add the item to your cart. Wait 48 hours. If you still want it, buy it. I’ve found that roughly half of what I nearly bought disappears from the list after two days — the urge was real but temporary.

41. Unsubscribe from all retail promotional emails

Promotional emails are designed to create purchase intent where none existed. You weren’t thinking about new trainers until that 30% off email arrived. Unsubscribe from all of them. You’ll find the things you actually need without prompting.

42. Buy secondhand first

For clothing, furniture, electronics, books, and children’s items, search Vinted, Facebook Marketplace, eBay, and Depop before buying new. Items in good condition are regularly available for 20–80% less than retail.

43. Never shop when emotional

Retail therapy is a real phenomenon and a deliberately exploited one. Stress, boredom, and sadness all correlate with increased impulse spending. If you’re not in a neutral emotional state, put the phone down.

44. Use cashback sites and extensions for everything online

Rakuten and TopCashback (rakuten.com / topcashback.co.uk) give you a percentage back on purchases at thousands of retailers. Installing the browser extension takes five minutes. You get paid for shopping you were already doing.

45. Buy things in season

Winter coats in spring, garden furniture in autumn, Christmas decorations in January — seasonal discounts are predictable. Buy for next year when prices are lowest rather than when you need it.

46. Repair before replacing

A broken zip, a cracked phone screen, a heel that’s worn down — these are all fixable for a fraction of replacement cost. We’ve been conditioned to replace rather than repair. Most repairs take 20 minutes and cost £5–£20.

47. Avoid the supermarket’s eye-level shelves

Premium products are positioned at eye level because they’re the most profitable for the supermarket, not the best value for you. The cheaper own-brand equivalent is usually one shelf below. Look down.

48. Track every purchase for 30 days

This sounds tedious but it’s the single most important awareness exercise in personal finance. You will find spending you didn’t know you were doing. Every person I know who has done this properly has been surprised by at least one category.

Eating Out and Entertainment — Save $70–$100/Month

I’m not going to tell you to stop going out entirely. That’s the kind of frugal advice that makes people give up on frugal living because it turns a financial strategy into a joyless existence. The goal is to spend intentionally, not to spend nothing.

49. Cook at home six nights a week

One meal out per week is a treat. Six meals out per week is a habit with a significant price tag. Even cooking simple meals at home the majority of the time saves £100–£200/month for a couple compared to regular restaurant dining.

50. Take advantage of lunch deals instead of dinner

Most restaurants offer the same menu for significantly less at lunch. A meal that costs £25 per person for dinner often costs £12–£15 for the same dishes at midday. Same quality, different price.

51. Use TOTUM, Student Beans, or available discount cards

If you’re a student, your card unlocks genuine discounts at hundreds of retailers, restaurants, and services. I’ve used mine more times than I can count. If you’re not a student, similar discount programmes exist — check what’s available in your area.

52. Use your local library

Libraries give you free access to books, audiobooks, films, magazines, and often digital services like Libby for e-books and audiobooks. I read 3–4 books a month through my library. The saving versus buying each one is around £30–£40/month.

53. Find free local events

Free museums, park concerts, community markets, food festivals, outdoor cinema — most cities and towns have a calendar of free events. I check local Facebook groups and council websites regularly. Some of my best experiences have cost nothing.

54. Host rather than go out

A dinner party at home costs a fraction of the equivalent restaurant bill for the same number of people. Cooking for friends is sociable, intentional, and genuinely more enjoyable for many occasions than a noisy restaurant.

55. Cancel streaming services you’re not watching

Most people have 2–4 streaming subscriptions they rotate between. Keep the one you’re actively watching, cancel the others, and rotate quarterly. You won’t run out of things to watch and you’ll spend £10–£30 less per month.

Debt and Banking — Save $60–$100/Month

This is the category most frugal living guides underweight. Interest on consumer debt is one of the most significant drains on a household budget — and unlike most spending, it’s invisible until you look for it.

56. Pay more than the minimum on credit card debt

At 20–26% APR, a £3,000 credit card balance paying only the minimum costs around £700–£800 per year in interest alone. Paying an extra £50–£100/month on top of the minimum dramatically accelerates payoff and reduces total cost.

57. Use the debt avalanche method

List your debts from highest interest rate to lowest. Pay minimum on all but the highest-rate debt — throw every extra pound at that one. When it’s paid off, move to the next. This is mathematically the fastest way to pay off debt.

58. Move credit card debt to a 0% balance transfer

If you have credit card debt at 20%+ APR, a 0% balance transfer card eliminates interest for 12–24 months. This is not a trick — it’s a legitimate tool. Use the time to pay down the balance aggressively, not to accumulate more.

59. Put savings in a high-yield account

A standard bank current account pays near-zero interest. High-yield savings accounts currently pay 4–5% APY. If you have £5,000 in savings, that’s the difference between £5 and £200–£250 per year in interest earned. Move the money.

60. Automate savings before you spend

Pay yourself first. Set up a standing order on payday that moves a fixed amount to savings before you see it in your current account. Money you don’t see, you don’t spend. The amount doesn’t matter at first — the habit does.

61. Avoid foreign transaction fees

If you travel or shop on foreign sites, a card with no foreign transaction fees (Monzo, Starling, Wise in the UK; Charles Schwab in the US) saves the typical 3% fee on every transaction. For regular travellers, this is significant.

62. Check your credit report annually

Errors on credit reports are more common than people realise and can cost you on interest rates when borrowing. Check your report free at Experian, Equifax, or TransUnion and dispute any inaccuracies.

Personal Care and Health — Save $60–$80/Month

Personal care is another category where convenience pricing is significant. Branded products are priced as much for their marketing as their efficacy. Generic equivalents often share identical formulations.

63. Buy generic over-the-counter medication

Paracetamol, ibuprofen, antihistamines, antacids — the active ingredients are identical in own-brand and premium versions. The packaging is different. The price can be 10x different. Buy the cheapest version with the same active ingredient.

64. Use price comparison for prescriptions

In the US, GoodRx and similar services show the actual price of prescriptions at different pharmacies. The variance can be dramatic — sometimes 80%+ for the same medication. Always check before paying.

65. Make your own basic cleaning products

White vinegar, bicarbonate of soda, and washing-up liquid clean effectively and cost a fraction of branded cleaning products. A spray bottle of diluted white vinegar cleans glass, surfaces, and limescale. It works because of chemistry, not marketing.

66. Buy beauty and hygiene products in bulk

Shampoo, conditioner, moisturiser, shower gel — these don’t expire quickly. Buying a larger size or in bulk from Costco or a wholesaler saves 20–40% versus buying single-use sizes repeatedly.

67. Switch to a safety razor

A good safety razor costs £20–£30 and the blades cost pence each. Cartridge razors are one of the great consumer product markups — the handle is cheap; the blades are what they make money on. A safety razor pays itself back within months.

68. Use sunscreen as your moisturiser

A two-in-one SPF moisturiser replaces two products. Skincare can be genuinely simple: a cleanser, an SPF moisturiser, and an evening moisturiser covers most people’s needs for significantly less than a 10-step routine.

69. Cancel the gym and exercise for free

Running, cycling, bodyweight training, and yoga all have zero marginal cost. If you genuinely use a gym frequently, keep it. If you’re paying £40–£80/month for occasional visits, the cost-per-use doesn’t work.

Infographic: 10 spending traps companies use — and the system fix for each one

Mindset and Systems — The Tips That Make Everything Else Work

These aren’t spending tips — they’re structural changes that make all the other tips stick. From my digital marketing studies: the reason most people fail at frugal living isn’t a lack of knowledge about what to do. It’s a lack of systems that make the right behaviour automatic.

70. Write a monthly budget every single month

A budget isn’t a restriction — it’s permission to spend on the things you’ve decided matter. Without one, spending drifts. YNAB (youneedabudget.com) is the best budgeting tool I’ve encountered. Mint does the basics for free.

71. Know your “per hour” cost of purchases

Divide any purchase by your after-tax hourly wage. A £150 jacket is 5 hours of work. Is it worth 5 hours of your life? This reframe makes spending decisions feel concrete rather than abstract.

72. Do a monthly no-spend challenge

One month per year, commit to buying nothing beyond absolute essentials. No takeaways, no online shopping, no non-essential purchases. It resets spending habits, proves what you can live without, and typically saves £200–£400 in a single month.

73. Unfollow accounts that create want

Social media is full of aspirational content that functions as advertising. People you follow who consistently show you things to buy are costing you money. Unfollow them. This is not a small thing — social comparison is one of the biggest drivers of unnecessary spending.

74. Define your values before your budget

Frugal living that aligns with what actually matters to you is sustainable. Frugal living that asks you to sacrifice things that genuinely matter leads to failure. Decide your priorities first: what are the things in your life where more money spent does improve your happiness? Protect those. Cut everything else.

75. Understand the psychology of spending

Books like Predictably Irrational by Dan Ariely and Influence by Robert Cialdini explain how companies engineer spending decisions. Once you understand the mechanics, you’re much better at resisting them.

76. Celebrate progress without spending to celebrate

Reached a savings goal? Paid off a debt? The natural instinct is to reward yourself by spending — which is exactly the pattern frugal living is trying to break. Find non-spending ways to mark progress: a meal cooked with an ingredient you’ve been saving, an activity, a conversation.

More Tips — 77 to 101

Here are the remaining 25 tips in shorter form, organised by category. Each one makes a real difference — the collection is what builds toward $1,000/month.

More Food and Kitchen Tips

77. Use your spice rack to make cheap cuts of meat taste excellent

Cheap cuts braised low and slow are often better than expensive ones cooked quickly. Shoulder, shin, and brisket are consistently cheaper than fillet and sirloin.

78. Learn five cheap meals you genuinely enjoy

Lentil dhal, pasta e fagioli, egg fried rice, bean chilli, shakshuka. Each costs under £1 per serving. Knowing them by heart means you default to cheap on a tired weeknight rather than to delivery.

79. Grow herbs on your windowsill

A pot of basil, rosemary, and mint from the garden centre costs £3 each and lasts indefinitely. Fresh herbs from supermarkets cost £1 per week and die within days. The difference over a year is significant.

80.Drink tap water instead of squash or juice

A 2-litre bottle of orange juice costs £1.50 and has more sugar than a can of Coke. Tap water is free. If you want flavour, a slice of lemon or lime in a jug of water is barely more expensive.

81. Check unit prices, not package prices

The bigger package is usually better value per unit — but not always. Supermarkets are required to display unit prices (price per 100g or per litre). Always check the small print, not the headline price.

82. Plan meals around what’s on sale that week

Check your supermarket’s weekly offers before planning your meals, not after. Build the week’s menu around what’s discounted rather than shopping for a pre-set menu.

83. Use up leftovers before cooking fresh

“Fridge soup” — broth made from vegetable scraps, leftover protein, and whatever’s about to turn — is one of my favourite frugal habits. It tastes good, costs nothing, and means nothing goes to waste.

More Household and Utilities Tips

84. Insulate draughty windows and doors

Draught-proofing windows and doors costs £20–£50 in materials and can save £25–£50/year in heating costs. The payback is fast and the work is straightforward.

85. Use a programmable or smart thermostat

Setting your heating to come on 30 minutes before you wake rather than running all night makes a measurable difference. Smart thermostats (Nest, Hive, Ecobee) typically save 10–20% on heating bills and pay back their cost within 1–2 years.

86. Full loads only for dishwasher and washing machine

Running a half-full machine is the same energy cost as a full one. Wait until you have a full load. This halves the number of cycles — and therefore the energy and water cost.

87. Fix dripping taps immediately

A dripping tap can waste 15 litres of water per day — 5,500 litres per year. On a metered supply, that’s a real cost. A new washer from a hardware shop costs £0.50 and takes 10 minutes to fit.

More Shopping and Money Tips

88. Never pay full retail for electronics

Refurbished electronics from Apple Certified, Amazon Renewed, or reputable refurbishers are typically 20–40% cheaper than new and come with warranties. I’ve bought refurbished laptops and phones for years. The difference is cosmetic at most.

89. Negotiate salary increases regularly

Earning more is the other side of the frugal equation. A 5% raise on a £30,000 salary is £1,500/year — more than most other tips on this list combined. The average employer doesn’t offer raises proactively; you have to ask.

90. Use a rewards credit card — paid off in full monthly

If you have the discipline to pay the full balance every month, a cashback or points credit card earns money on spending you were going to do anyway. The moment you carry a balance, the interest costs more than any reward earned. This tip is conditional.

91. Check if you’re eligible for any government benefits

Tax credits, council tax reductions, free prescriptions, housing benefit — many people don’t claim what they’re entitled to. Entitledto.co.uk checks eligibility in minutes.

92. Audit your mobile phone plan yearly

Most people pay for more data than they use. Check actual usage in phone settings and switch to a matching plan. SIM-only contracts on Smarty, Giffgaff, or Lebara often cost £5–£12/month.

More Mindset and Lifestyle Tips

93. Define wants vs needs before every purchase

A want is something you’d like to have. A need is something you cannot reasonably function without. Most purchases are wants. That’s not wrong — but calling them what they are makes the decision more conscious.

94. Find free hobbies that you genuinely enjoy

Running, hiking, wild swimming, reading, cooking, drawing, writing — all cost nothing or close to it. I’ve found that the hobbies I most enjoy are largely free ones. The expensive hobbies are often the ones I took up because they seemed impressive, not because they brought me genuine satisfaction.

95. Talk about money openly with your partner

Financial incompatibility is one of the leading causes of relationship stress. A joint budget conversation once a month takes 30 minutes and prevents a significant number of arguments, resentments, and misaligned spending decisions.

96. Avoid lifestyle inflation after a pay rise

When your income increases, the temptation is to upgrade your lifestyle proportionally. This is how people earn more and save no more. Direct at least half of any pay increase to savings or debt repayment before adjusting spending.

97. Build a £1,000 emergency fund first

Before investing, before aggressive debt payoff, before anything else: build a basic emergency fund. Without it, any unexpected expense — car repair, boiler, medical — goes straight on a credit card. With it, you absorb shocks without compounding debt.

98. Read personal finance books (from the library)

The Total Money Makeover by Dave Ramsey, Your Money or Your Life by Vicki Robin, and I Will Teach You To Be Rich by Ramit Sethi — all free from your local library. These changed how I think about money more than any tips list.

99. Teach your children about money early

Children who understand the value of money, how saving works, and how to distinguish wants from needs develop better financial habits as adults. It’s one of the highest-return investments a parent can make.

100. Review your progress monthly — not obsessively, but consistently

A monthly review of your budget takes 15 minutes. What did you spend? Where did you overspend? What worked? What will you adjust? Consistency compounds. A year of monthly reviews changes financial behaviour more than any single insight.

101. Give frugal living time to work

None of this is instant. Month one of any frugal overhaul looks modest. Month six looks meaningful. Month twelve changes your financial picture in ways that are genuinely hard to believe when you’re starting. The people who fail at frugal living almost always fail in month two or three — just before the compound effect kicks in.

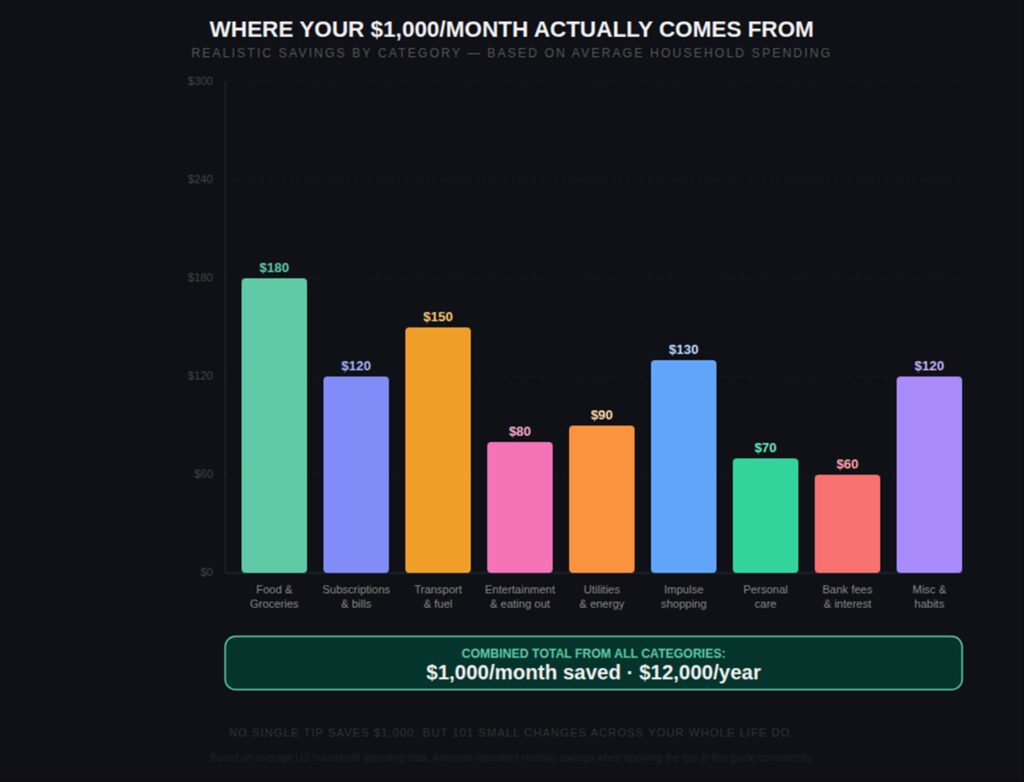

How the $1,000 Month Actually Adds Up

I promised at the start to show you the maths. Here it is:

- Food and groceries (switching to Aldi, meal planning, reducing waste): $150–$180/month

- Subscriptions and bills (cancelling unused, negotiating, switching supplier): $100–$130/month

- Transport (fewer car trips, comparing insurance, advance booking): $100–$150/month

- Utilities (energy habits, switching supplier, LED bulbs): $80–$100/month

- Impulse shopping (48-hour rule, secondhand first, unsubscribing from retail emails): $100–$130/month

- Eating out (cooking at home more, lunch not dinner, free events): $70–$90/month

- Debt interest (avalanche method, 0% transfer, paying more than minimum): $60–$100/month

- Personal care (generic medication, bulk buying, free fitness): $50–$70/month

- Miscellaneous habits (daily coffee, bottled water, library vs bookshop): $40–$60/month

Combined low end: $750/month. Combined high end: $1,010/month.

And that’s before factoring in earning more — a side hustle, a pay negotiation, selling things you no longer need. The $1,000 figure is real. It just requires breadth rather than depth: a little from many categories rather than a lot from one.

The most important single action: audit your subscriptions and switch to Aldi for staples. Those two changes alone typically save £50–£100/month and take under an hour. Do them before anything else on this list.

Frequently Asked Questions

Is frugal living the same as being cheap?

Not in the way I use the term. Being cheap means refusing to spend even when spending makes sense. Frugal living means spending intentionally — only on things that provide genuine value, and as efficiently as possible. A frugal person spends well on things that matter; a cheap person just doesn’t spend. The distinction is important for sustainability.

Where do I start if I’m completely new to this?

Three things: (1) Spend 20 minutes going through your bank statements and cancelling subscriptions you don’t use actively. (2) Start a grocery list before every shop and stick to it. (3) Open a separate savings account and set up a £25 or £50 automatic transfer on payday. These three actions alone will have a visible impact by month two.

Can I really save $1,000 a month on an average income?

On a median US income of around $56,000 (about $3,500/month after tax), saving $1,000/month requires cutting spending to around $2,500/month — which is achievable but tight depending on housing costs. In lower cost-of-living areas or shared housing, it’s more accessible. In expensive cities, you may find $500–$700/month more realistic. The $1,000 figure is a target showing what’s theoretically achievable across all categories, not a promise that it’s easy for everyone.

Will frugal living make me miserable?

Badly implemented, yes. Frugal living that removes all enjoyment isn’t sustainable — and it’s also not the goal. The goal is to spend money on the things that genuinely improve your life and stop spending it on things that don’t. Most people, when they actually track their spending, find significant amounts going to things they don’t value. Cutting those doesn’t cause misery. It often causes relief.

What’s the one thing that made the biggest difference for you?

✍ YOUR ANSWER HERE: What was the single frugal change that had the most impact on your student budget? Was it switching to own-brand food? Cutting a subscription? Starting to track spending? This specific personal answer is the most valuable thing you can add to this FAQ.

The Bottom Line

✍ YOUR CLOSING: Where does frugal living fit in your actual life as a student? What surprised you most about your own spending when you first started paying attention? Close with something true and specific — not a summary of the article but a genuine personal reflection. That’s what people remember.

Frugal living isn’t about deprivation. It’s about deciding that your money represents your time and energy, and refusing to let it go towards things that don’t deserve it.

The 101 tips in this guide aren’t a prescription — they’re a menu. Pick the ten that fit your life right now and do them consistently for three months. Then review, adjust, and add more. That’s it.

The $1,000/month figure is achievable. Not through any single dramatic change, but through the patient, unglamorous accumulation of small, smart decisions made over and over again until they become the way you live.